When you start the process of looking to buy a new home you find out pretty quickly the financing portion of the process is the most important. There are many types of Home Loans you can look at but almost all of your loan options will end up being some version of the three major loan types Conventional, FHA, or VA.

While anybody can apply for a conventional or FHA loan, the VA loan differs. The VA loan is a special type of loan that is reserved for veterans; active duty service members including members of the Army, Navy, Air Force, Marines, Coast Guard and National Guard, military spouses, and the surviving spouse.

We work in the Colorado Springs real estate market. Because Colorado Springs is such a great military town, we have a lot of experience with the VA Home Loan. Colorado Springs is home to The Fort Carson Army Base, Peterson Air Force Base, Schriever Air Force Base, U.S. Northern Command, and the United States Air Force Academy.

This abundance of VA eligibility has taught our team how to work with VA Home Loans, military home buyers, first time military homebuyers, and military veterans. Now let’s take a look at the VA loan.

What is a VA loan?

Simply put, a VA loan is a mortgage loan that is backed by the U.S. Department of Veterans Affairs (a.k.a. VA). The VA is a federal government agency established to support Veterans as well as active-duty members. Along with the GI Bill, the VA loan program was created in 1944 and signed into law by President Franklin D. Roosevelt as a benefit for active-duty military members, veterans, reservists, National Guard Members, and surviving spouses (until they remarry).

Types of VA Loans:

There are a couple of different types of VA mortgages. Let’s look at the various types of available VA loans.

VA Backed Purchase Loans

This is the most common type of VA loan. The name VA loan can be misleading because the VA doesn’t actually loan the money for this program, they simply guarantee the money loaned by private lenders. The veterans administration acts as a backstop for the lender for loss in the event the borrower defaults on the loan. The actual loan is made by private banks, a credit union or mortgage lenders. The process is much like the conventional and FHA loans; the only difference is the VA acts as the mortgage insurer. Like other loans, the VA loan can be either a fixed rate mortgage or an adjustable rate mortgage.

Native American Direct Loan (NADL) Program

In this program the VA actually loans the money acting is the lender and or bank. these loans are only available to eligible Native American Veterans looking to purchase, build, or improve a home on Federal Trust land or to reduce their current interest rate.

Interest Rate Reduction Refinance Loan (IRRRL)

This mortgage product is a VA backed refinance program for eligible property owners with an existing VA loan. The interest rate reduction refinance loan allows the borrower to reduce their monthly payments, or stabilize their payments. This is a great option if you’re looking to improve your loan terms.

Cash-Out Refinance Loan

This is a refinance option backed by the VA that allows the borrower to replace their current loan with potentially better terms. Additionally, this is a good way to tap into your existing home equity in order to take cash out for repairs, updates, and potentially paying off other higher interest debt.

VA Construction Loan

The VA does offer backing on a 0% down construction loan. Construction loans are considered risky, due to the fact that there is no existing home to foreclose on should the borrower default. Because of those few lenders are willing to take the risk associated with these loans. We generally see borrowers take out a construction loan from the home builder or a local lender and then refinance into a permanent VA loan once the home is finished.

Benefits of a VA Loan

The VA Backed loan is a benefit earned through military service and makes buying a home easier for those that qualify. The VA lowers the bar on downpayment requirements for borrowers while reducing the risk for the private lenders that make these loans. there are many additional benefits to this loan for eligible borrowers.

- No Downpayment – This is probably the most valuable part of the VA loan. With FHA and conventional loans requiring anywhere from 3% to 20% down payment, the no down payment feature of the VA loan is extremely valuable. Are the median home price in the United States is just over $300,000. This means if you were using an FHA or conventional loan you’re looking at having to come up with anywhere between $9,000 and $60,000 cash in order to make a down payment and even qualify for a loan. The lack of money for a down payment is the single biggest obstacle that keeps people from becoming homeowners.

- No PMI or MIP – PMI stands for private mortgage insurance, and MIP stands for mortgage insurance premium. These are both types of insurance policies purchased to protect the mortgage lender in the event the borrower defaults on their loan. In the case of a VA loan, the insurance for the lender is coming directly from the VA. The lender on a conventional loan is looking for a minimum of 20% equity in the property. This means your down payment would need to be at least 20% in order to avoid having to pay PMI. While on an FHA loan the Mortgage Insurance Premium is a permanent fixture.

- Higher Debt to Income Ratios – This is sometimes referred to as DTI or qualifying ratios. This ratio is a VA underwriting guideline that looks at the relationship between how much income you produce on a monthly basis as it relates to your housing expenses and major monthly debts. The ratio gives the VA lender insight into your ability to repay debt. To establish this number, the lender will look at the following debts:

- Mortgage Payment

- Additional shelter expenses

- Real Estate Taxes

- Hazard Insurance

- Any Special Assessments

- Any HOA or Condominium Fees

- Any significant recurring monthly debts/obligations

Once all of the pertinent debt information is established, the lender will identify and verify the income side of the DTI ratio. The lender’s job is to identify and verify there is sufficient income available to meet the following:

- Mortgage payment

- Other shelter expenses

- Debts and obligations

- Family living expenses

The lender looks for what they consider to be effective income. This means income that is determined to be verifiable, stable, reliable and is anticipated to continue into the foreseeable future. In order to determine if income can be considered “stable” the lender will look at the following:

- The borrower’s past employment record

- The borrower’s training, education, and qualifications for their current position

- Type of employment

Once all of the debt and income information is compiled the lender will divide the sum of the debt by the sum of the income in order to establish the ratio. They are looking for a number under 41 this means the monthly housing payments should not exceed 41% of gross monthly income.

It’s important to note that on a Conventional Mortgage or FHA loan two sets of ratios are used, Front End and Back End. The Front ratio looks at housing expenses only, while the back end ratio is all-inclusive, taking into account both housing expenses and major monthly debt. The VA only uses the back-end debt to income ratio.

On a VA Home Loan, lenders will take a more comprehensive look at your finances, especially when compared with loans underwritten for conventional guidelines. It is not uncommon to see VA underwriters accommodate debt-to-income ratios in excess of 60% when using the second tier of qualification, residual income.

Residual income is any remaining discretionary income after a homeowner has fulfilled their monthly credit obligations. While the VA guidelines state that a VA borrower’s DTI should not exceed 41% the VA can grant an exception, additionally if the applicant’s residual income is more than the VA’s minimum residual income guidelines by 20% or more, DTI can become a non-factor.

Refinance Options – In addition to the VA-backed purchase loan there are two popular options for refinancing your property as well. The first is The “Interest rate reduction refinance loan” also known as IRRRL. This is for VA borrowers that have an existing VA-backed home loan but are interested in reducing their monthly mortgage payments. The IRRRL allows the borrower to replace their current loan with a new one under more favorable terms.

Lower Interest Rates – Low rates and flexible mortgage options are two important characteristics of this type of mortgage. Because the VA loan is backed by the government, it is less risky than other loan types. This is why VA lenders are able to offer such competitive mortgage rates. According to mortgage data provider ICE Mortgage Technology when they examined 30-year fixed-rate loans closing in November of 2020, VA loans had an average rate of 2.72%, compared with 2.99% on a conventional mortgage for the same term.

Flexibility after Bankruptcy and Foreclosure – VA loans do offer you the ability to qualify for your VA loan benefit even after bankruptcy or foreclosure. In many cases, you will have a much shorter waiting period than you would for a conventional loan. You may be eligible for a VA Loan in two years after a Chapter 7 bankruptcy is discharged, and one year after filing for a Chapter 13 bankruptcy. It generally takes two years after a foreclosure but some lenders have no required waiting period after a short sale.

This is certainly better turn the 4 to 7 years you would need to wait before being able to fly again with a conventional loan.

Drawbacks to a VA Loan

- Funding Fee – The funding fee is a one-time fee paid to the Department of Veterans Affairs. The funding fee helps lower the cost of VA loans for U.S. taxpayers because a VA home loan program requires no down payments or monthly mortgage insurance. It is possible to reduce your funding fee by coming up with a down payment on your home. The table below shows how much you’ll pay based on your downpayment and whether or not you’ve used the program before. There are certain cases where the VA borrower does not have to pay the funding fee, for example, those with service-related disabilities, surviving spouses, and purple heart recipients.

| Downpayment | 1st Time VA Borrower | Repeat VA Borrower |

| < 5% | 2.63% | 3.6% |

| 5% to 10% | 1.65% | 1.65% |

| 10% or more | 1.4% | 1.4% |

- Home Sellers Don’t Like Them -Many home sellers are opposed to selling to a buyer with a VA Loan. This is because they mistakenly think that they will be responsible for paying all of the buyer’s closing costs. While the VA does limit which closing costs Veterans are allowed to pay, The home sellers are not required to pay any of those closing costs for the VA home buyer, this includes those “non-allowable” fees that Veterans aren’t allowed to pay.

- VA Loans are Only For a Primary Residence – A VA-backed purchase loan is intended for the purchase of a veteran’s primary home. VA borrowers are expected to live in the properties they purchase. The VA has developed occupancy requirements in order to make sure that homeownership is the buyer’s intended purpose, these loans should not be used to purchase a rental home, investment properties, or a vacation home. There are exceptions based on employment situations for those no longer on active duty, and you should check with your Regional Veteran’s Administration Center if you find yourself in this situation. Active service members can also provide the VA with something called “valid intent to occupy” this is used when the homeowner is deployed away from their permanent station of duty and maybe renting the home out while they are away.

VA Loan Eligibility

The Department of Veterans Affairs (VA) establishes the basic service requirements needed to qualify for VA loan eligibility. Additionally, the loan applicant will need a valid Certificate of Eligibility (COE) and will need to meet the lender’s income and credit requirements.

The income and credit requirements are not mandated by the VA, interest rates are established by the particular lending institution you are working with. These numbers can change based on the companies tolerance for risk and factors like your credit score.

Eligibility depends on the amount of time you spent on active duty if you are a military veteran, and how you separated from the military. You can check the VA website for more specific requirements. Beyond these requirements, to obtain a VA-backed home loan, you’ll also need to meet your lender’s credit and income loan requirements.

Certificate of Eligibility

The Certificate of Eligibility is an actual document that confirms for a VA lender that you actually qualify for a VA-backed home loan. This document also shows the amount of entitlement you have available to use.

You will need a certificate of eligibility, visit the VA website to learn more about obtaining your Certificate of Eligibility.

Entitlement

$144,000 is significantly below median home prices in most parts of the United States. In order for the VA to ensure veterans could still have access to homeownership, they decided to tie their guaranty amounts to the conforming loan limit for conventional mortgage financing. This decision created the secondary or bonus layer of entitlement for those needing to borrow more than $144,000.

This secondary layer looks at the conforming loan limits for the particular county you are buying in. As of 2021 the conforming loan limit for most of the United States is $548,250.

Since the VA usually commits to cover 25% of the loan amount. $137,062 would be the entitlement amount or 25% on a $548,250 loan amount. If you meet the minimum loan requirements, most lenders will loan you up to four times the amount of your basic entitlement towards your purchase price without requiring a down payment.

Your available entitlement amount will be on your Certificate of Eligibility. If you have previously used your VA Loan, the entitlement amount on your COE may be less than you expect. Any entitlement you have previously used in connection with a VA backed home loan can be restored once the property you have previously used your VA Loan for is sold, and the loan has been paid off. In the event of a loan assumption, an eligible veteran-transferee would need to agree to assume any outstanding balance on a VA loan and substitute their entitlement for the amount you had originally used on this loan. The assuming veteran-transferee would also need to meet the occupancy, income, and credit requirements of both the Veterans Administration and the private lender.

VA Loan Limits

Since their inception VA loans have had a loan limit, these limits no longer apply, at least to qualified veterans that have their full VA loan entitlement. A qualified veteran with full entitlement can borrow as much as the private lender is willing to loan. On the other hand, qualified borrowers with reduced or a partial remaining entitlement would still be subject to VA loan limits. If you have a less-than-full entitlement, you probably have one or more existing VA loans. In some cases, your entitlement may have been reduced because of a default on a previous VA loan.

If you’re interested in obtaining a VA loan but have reduced entitlement, you’ll need to check with your lender to find out how much you qualify for without coming up with a down payment.

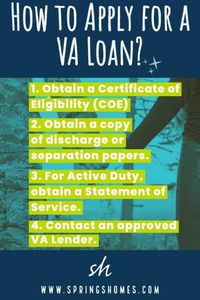

How To Apply

How To Apply

The first step in the application process for a VA loan is to obtain your Certificate of Eligibility (COE). This document shows the lender you are working with that you do qualify for this benefit. If you’re a Veteran, you are also going to need a copy of your discharge or separation papers (DD214). Currently, active-duty service members will need to obtain a statement of service, this should be signed by your commander, adjutant, or personnel officer.

Once you have obtained the appropriate documentation, you need to contact a mortgage lender that is an approved VA lender. Your real estate agent can usually recommend a good VA-approved lender.

Because the lender is actually making the loan they are going to go through the same process they use for any other mortgage loan in terms of making sure you qualify. They will pull a credit report, verify your employment status, and need to look at your tax returns in order to make sure you qualify for the loan. Since the loan will most likely be sold into the secondary mortgage market, the lender needs to make sure the loan is written to those standards, otherwise, the loan becomes unsellable and the lender will need to keep it in their own portfolio reducing the money they have to lend.

Closing Costs

The VA loan is no different than any other home mortgage loan, it has closing costs. These fees can range on average between 3% to 5% of the loan amount. Other factors like taxes and insurance can impact your closing costs as well as your choice of lender.

- Origination Fee – The origination fee is one of the ways a lender makes money from the loan. Origination fees are essentially a one-time fee that allows the lender to keep their interest rates low while still making a profit. The VA does allow a lender to charge up to 1% of the loan amount for origination. This covers the cost of underwriting and processing the loan.

- The Appraisal Fee – You will be required to have an appraisal. This verifies for the lender as well as the VA, that the property is worth what you are paying for it. If the lender ends up having to take the property back due to non-payment, they want to know that they will be able to resell the property without a major loss. Appraisal fees for VA Loans are set by the VA, depending on where you live a VA appraisal can cost between $700 to $1,000. You can find out how much you can expect to pay for your VA appraisal by looking at the VA’s appraisal fee schedule on the VA’s website.

- Title Insurance – Your lender is going to require their own title insurance policy to protect them against any problems with the title like liens, legal defects, or other potential title clouds. This is in addition to the Title Policyowner’s title policy the Seller will most likely be offering the buyer.

- Discount Points – Discount points have become rare because interest rates have become so low. In a different environment, the buyer would have the option to pay points. This means they could buy down their interest rate by paying points. One point is equal to 1% of the loan amount. While paying points has become rare, it is still an option.

- Credit Report – Part of the qualification process for a VA loan involves looking at the applicant’s credit history. In order to do this, the lender will need to pull a credit report and the buyer may need to pay for it depending on the lender. The VA limits the cost of this report to $50. Many lenders will pay this fee for the borrower.

- Inspection Fees – There are inspections required by the VA. The type of inspection and who pays varies from region to region. For example, in Texas, a termite inspection is required and the seller pays for it. While in Colorado the VA requires a bacteria test for any property on a well, this is a buyer cost. Your lender can provide you with a list of required inspections and who is responsible for purchasing them.

- Funding Fee – We discussed the VA funding fee previously in the drawbacks portion of this article but it’s worth bringing up here under closing costs as well. VA borrowers have the option of rolling the funding fee into the cost of the loan. This avoids the initial financial hit of having to pay the fee upfront. Choosing this option makes the funding fee a portion of the loan and will increase your monthly payment for the life of the loan.

VA Loan Interest Rates

While the VA regulates many aspects of the cost of a VA Loan to the veteran, the interest rate is not one. Private lending institutions like banks and mortgage companies are responsible for determining their own interest rates. Your credit score will have the biggest impact on the interest rate the lender offers. VA Loans offer competitive interest rates and low to no down payment requirements because of the security of the VA’s backing of these loans. While VA loan interest rates are generally lower than traditional mortgage programs like Conventional and FHA mortgage loans, you can reduce the interest rate even further by having a strong credit history.

Required Credit Scores

Credit Scores, like interest rates, are not controlled by the VA. Private lenders on the other hand will have minimum credit score requirements. Unlike a traditional loan, the VA loan program offers some flexibility in credit requirements for their mortgage products. Potential borrowers don’t need to have perfect credit scores, we generally see attractive interest rates on VA loans for borrowers with credit scores in the 650 – 750 range. If your score is below this, you may still qualify but at a slightly higher interest rate. If your credit score is in the 500’s you may have problems qualifying but don’t give up. Most lenders have programs to get borrowers with poor credit back on track and into a VA loan.

In Conclusion

Once you understand what is a VA Loan, you begin to see that the VA loan is one of the most useful loan programs available to members of the Army, Navy, Air Force, Marines, Coast Guard and National Guard members, and an amazing benefit for eligible veterans, active duty members, and military families in general. If you have earned this benefit through your service, it certainly makes sense to take advantage of the program