What is homeowners insurance? A homeowners insurance policy protects you and your home against property damage and losses from events like theft, fire, catastrophes, natural disasters, and injury.

Homeowners insurance doesn’t refer to a single type of coverage, it’s more like an entire group of different types of policy features that all protect the same things; you, your belongings, and you’re home based on your specific requirements.

Homeowners insurance doesn’t refer to a single type of coverage, it’s more like an entire group of different types of policy features that all protect the same things; you, your belongings, and you’re home based on your specific requirements.

Because the needs of policyholders can be drastically different, homeowners insurance policies are offered in a wide range of policy types with different coverage levels, and options from basic bare-bones dwelling policies to full-scale comprehensive coverage.

In most cases, the type of policy you will need is going to be dictated by your mortgage lender, if you have one.

Is Homeowners Insurance Required?

The most common scenario where homeowners Insurance is required is when you are using a mortgage to purchase your home. Since the mortgage lender has so much money invested in your home, they want that investment protected.

Most mortgage lenders are going to require a replacement cost coverage policy, this is often referred to as a “Standard Policy”. In most cases, the lender will even make those payments, they do this from a prepaids escrow account that gets set up at the time of closing.

If you are paying cash, or own the home free and clear, there should be no requirements for homeowners insurance.

Even if homeowners insurance is not required, given the cost of rebuilding or repairing damages, it is certainly a good idea to protect your investments with some level of homeowners coverage.

The mortgage lender will want to know that the house can be rebuilt in case of any damage or destruction. Most lenders are going to require that the house is covered for 100% of its replacement cost.

Another scenario we see homeowners insurance requirements is in an HOA or Home Owners Association. When you live in a condo, there is a homeowners association to take care of all exterior maintenance issues and repairs. This association already has an insurance policy, but its policy will cover the structure of the building and other common areas.

Your individual unit is still your responsibility and you will not be protected by the association’s policy. In such a case, you can buy a separate policy for yourself that will protect your personal belongings. Should there be a theft, damage, personal injury, or any other incident, you can make a claim and get coverage.

Property managers and landlords will often require that their tenants purchase a renter’s insurance policy because it provides an extra level of protection for the homeowner. Renters insurance is considered a form of homeowners insurance. This policy protects the renter’s belongings and provides liability coverage against injuries that occur on the property as well.

How Does Homeowners Insurance Work?

Homeowners insurance offers coverage against loss or liability in three major categories:

- Damage to the exterior and interior of the property – In the event your home is damaged or destroyed by fire, hurricane, lightning strike, or another covered peril, your insurance company would compensate you for the repair or rebuilding of your home. This is called a covered loss and includes other structures located on the property like sheds’ barns and fences.

- Damage or loss of personal belongings – This includes things like clothes, furnishings, appliances, and much of the other stuff in your home are covered if they’re destroyed by a covered peril. It is also possible to add “off-premises” coverage to your policy, this enables you to file a claim no matter where the loss occurs.

- Liability for accidents or injuries that occur on the property – Provides protection from lawsuits filed by others. This clause even protects from liability issues related to your pets!

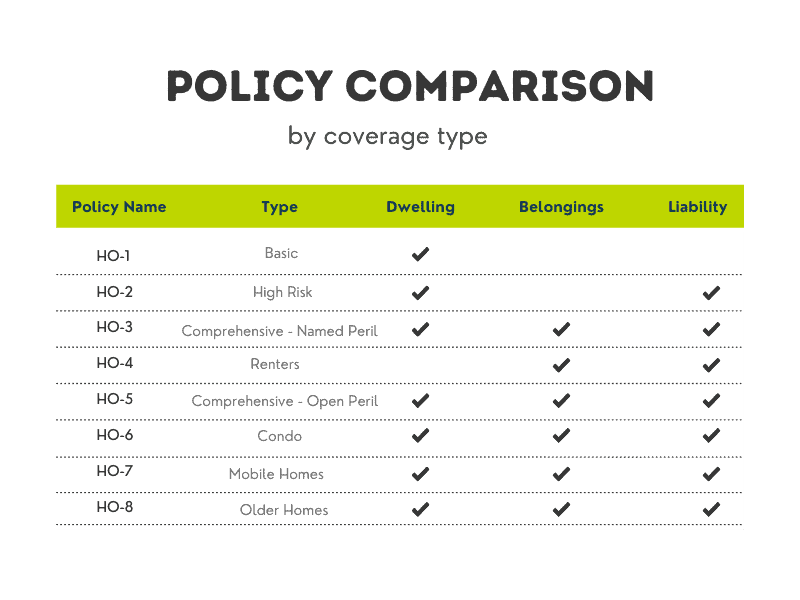

A standard policy should cover all four of these categories, while other policy types may only cover certain portions of this list. For example, a renters policy only covers belongings and liability, not dwelling, while an HO-1 policy only covers the dwelling.

In addition to paying for repairs, or replacement, a standard policy should also pay for temporary lodging while repairs are being made to the home.

Not all homeowners insurance policies offer the same level of coverage. There are actually eight different types of policies, these run the gamut from basic to comprehensive.

What is Not Covered?

Homeowners Insurance covers a wide range of situations and scenarios but there are some events and situations that are usually excluded from coverage.

- Acts of God – This would be considered as an event that happens which is outside the realm of human control, or can’t be predicted or prevented. Events like earthquakes, hurricanes, and floods are all considered acts of God.

- Acts of War – This refers to any loss resulting from events like war, invasions, insurrections, riots, strikes, or terrorism. There is specific insurance to cover these types of events. Acts of war are excluded from standard insurance policies due to the high risks involved. There are war risk insurance policies available.

There is also a category of perils or events that are not included on a standard policy but can be covered with additional coverage riders. For example, hurricanes, earthquakes, and floods all require separate coverage at an extra cost.

Actual Cash Value vs Replacement Cost

Another important aspect of homeowners insurance is the way the policy actually pays for damages, Actual Cash Value (ACV), or Replacement Cost.

Under the replacement cost model, the insurance company simply pays for the replacement of the item with a new or comparable item. It doesn’t matter what age or condition the item was in at the time of the claim.

In an actual cash value (ACV) scenario, the insurance company will depreciate the item for things like age or wear and tear. This type of policy essentially pays out what the item was worth at the time of the claim.

For example, if your 10-year-old roof is totaled by a hail storm, the insurance company will pay for the replacement but will subtract for the age of the roof. Let’s say $5,000 is the depreciation estimate, and your deductible is $2,000. On a $12,000 roof replacement, your share of the cost would be $7,000 and the insurance company would pay the remaining $5,000.

The 8 HO Policy Types

There are eight common levels of homeowners insurance coverage, HO-1 through HO-8. These policies are used for different types of situations. For example, an HO-1 is a basic policy that provides dwelling coverage only, while HO-4 is strictly for renters.

These policies are very similar in terms of what they cover, the difference has to do with something called perils.

What are Perils?

Peril describes a specific cause of damage or injury that relates to a property or people on the property. There are two types of perils “named peril, and “open peril”, named perils consist of 16 events that an acceptable homeowners policy should cover.

Named Perils

Here is a list of the “16 Named Perils” found in most standard homeowners insurance policies:

- Fire and/or lightning

- Windstorm and/or hail

- Explosion

- Riots

- Aircraft

- Vehicles

- Smoke

- Vandalism

- Theft

- Falling objects

- Weight of ice, snow, or sleet

- Accidental discharge or overflow of water or steam

- Sudden and accidental tearing, cracking, burning, or bulging

- Freezing

- Sudden and accidental damage due to short-circuiting

- Volcanic Eruption

Open Perils

Open perils a.k.a. “All Perils” is everything else that could cause damage, minus any exceptions the insurance company places in the policy.

An HO-5 policy is an open peril policy that provides you with the highest level of protection. In this policy, unless the peril is specifically excluded by the insurance company, it’s covered.

A good example of a named exclusion would be “Construction Defects”. Let’s say the fireplace in your new home was incorrectly installed. This improper installation results in flames and smoke causing damage to the home. A standard homeowners insurance policy would not cover the fireplace but it would cover the damage to the home from the smoke and flames.

It is common to see “open perils” associated with the dwelling portion of an HO-3 homeowners policy while the personal property side of the policy that covers the rest of your belongings is named peril.

It is possible to add open perils coverage to a standard policy but with a higher insurance premium.

Dwelling Coverage

Dwelling coverage is the foundation of most homeowners insurance policies and is the only lender requirement. The mortgage lender will require that the dwelling coverage portion of your homeowners insurance policy covers the replacement cost In most cases this will require an HO-3 policy.

In the case of dwelling coverage for a standard homeowners policy, depreciation isn’t used to calculate the payout. The insurance company will pay to rebuild using materials of similar quality.

The cost of the insurance policy will actually be included in your mortgage payment. If on the other hand, your loan to value ratio is low, you will have the option to pay your premiums separately. However, your lender will probably charge you extra fees for this option.

Liability Coverage

Liability insurance helps the policyholder cover medical bills and repair costs if they are responsible for another person’s injuries or property damage.

This coverage is also available to renters in an HO-4 renters policy, it helps cover legal expenses if the renter gets sued over an incident that occurs in the rental property.

Renters often assume that the landlord’s insurance policy will cover any issues they have at or on the property, this is incorrect. The landlord should have a separate policy that protects them and their interest in the property only. The liability portion of that policy protects them from liability issues .that arise with the tenant and that relate to negligence on the landlord’s behalf.

While a visitor to the property might have a case against the landlord in the event of their negligence, the brunt of the liability would come down on the renter, not the landlord. this is why many landlords and property managers make a renter’s policy mandatory for their properties.

There are policy limits to the amount an insurance policy will cover. Standard liability limits tend to be $100,000, the policyholder does have the option of purchasing a higher limit. You should discuss your situation and your potential needs with your insurance agent. It is better to be overinsured than underinsured.

Personal Property Coverage

Personal property coverage is for your personal belongings. This covers things like your furniture, clothes, electronics, and other personal items. If the claim is for a covered loss the coverage extends to anywhere in the world you suffer the loss.

Deductibles

Most homeowners insurance policies have a deductible which the policyholder pays in the event of a claim. The deductible is out-of-pocket money the policyholder pays before the insurance pays.

There are different theories about why insurance companies require deductibles, the most likely reason is that the policyholder has some financial responsibility for the claim. The idea is the deductible means the policyholder it’s serious because they have some skin in the game.

Let’s say you have a roof claim due to a hail storm. The roof replacement will cost $12,000 and you have a $2,000 deductible. Your portion of the new roof is $2,000 this comes out of your own pocket, and the insurance company will pay the balance of $10,000.

It is important to note that you have control over how much you want the deductible to be. As a general rule, the more expensive the policy, the lower the deductible.

Recoverable Depreciation

Many replacement cost homeowners policies have a recoverable depreciation clause. Recoverable depreciation is the difference in cost between the actual cash value of the claim and the replacement value.

If your replacement cost policy has a recoverable depreciation Clause, the insurance company will pay you the actual cash value amount upfront. Once the repairs are complete oh, they will pay the remaining recoverable depreciation cost.

Insurance companies do this to cut down on fraud. It’s not uncommon for homeowners to use the check they receive for a roof replacement to buy a new car or go on vacation. This doesn’t become a problem for them until they try to sell the home and upon inspection find out that the roof wasn’t replaced, and the insurance money for the roof replacement was used on a trip to Disneyland.

Using recoverable depreciation helps minimize the insurance company’s losses from fraud.

Shopping Around for a Policy

Lenders do require you to buy a home insurance policy, but they provide you with the freedom to choose any provider you like. There are many insurance companies that charge varying rates and provide you with different coverage levels.

Before you choose a provider, compare them on the basis of a number of factors such as the coverage levels, the premium amounts, deductibles, and so on. Needless to say, a policy available at a lower rate will not always be a great choice because it may not provide you with adequate coverage. Also, review their claim policies and make sure you are satisfied with the terms. How To Save On Home Insurance and Still Get the Most Out of It.

Factors that Can Affect Your Premiums

Roof

The condition of your roof has a direct effect on your premiums. If your roof is made from a material that resists impact, you can get a discount of up to 20% for your premium rates.

In some cases, a roof can be considered uninsurable such as when you have a t-lock or wood shake roof. Should this be the case, you may have to replace the roof or exclude the roof from your policy.

Electrical Systems

A roof must pass the qualifications of your insurance provider, but this is not exactly the case with electrical systems. The only condition required by Insurance companies is that the electrical system meets current codes and should have been updated once in the last 25 years.

Location of the Fire Department

Surprising as it may seem, this does affect your premiums. If the fire department is more than a couple of miles away, your rates could be higher.

Home Age and Construction

If your home is old or bigger, you will have to pay higher premiums. Construction material also affects the rates; masonry and brick homes reduce premiums since they can reduce the damage caused by fire or wind.

Deductibles

We have already mentioned this; if you agree to pay a higher deductible, your premiums will reduce.

There are other factors a well which can affect premiums such as your credit scores, insurance claims history, and the location of your house.

Other Insurance Policies Which You May Need

Flood Insurance

Administered by the Federal Emergency Management Agency or FEMA, a flood insurance policy is required at an additional cost if you live in an area that is prone to flood. If risks of flood damage are high, lenders may make it mandatory to obtain flood coverage. Flood coverage is not included in a standard homeowners insurance policy. Many providers offer it if requested by the homeowner. If your carrier does not offer flood insurance, you may purchase a policy through FEMA.

Some water damage is covered by homeowners insurance, as long as it is not due to flooding. For example, if a water heater bursts and causes water damage to your personal items or nearby sheetrock, the damage would be covered.

Earthquake Insurance

Although not historically an issue here in the State of Colorado, it is still worth mentioning. An earthquake is another incident that is not covered by a standard homeowners insurance policy. If you live in an area where quakes are frequent, you may want to buy this policy. However, you will have to pay a deductible amount that is higher than what you will have to pay for the standard policy.

The HO-3 policy is becoming the most popular policy for new homeowners in spite of being a named perils policy. Policyholders can upgrade the policy to remove the named perils and essentially make this policy more similar to an HO-5 without the cost.

Keeping Up With Your Policy

It’s important that you keep your homeowners insurance policy current. This means as you make improvements or the price of your house increases, you should increase the coverage of your policy.

Experts recommend reviewing your insurance policy annually. This means taking a detailed look at your policy, and coverage limits. Your insurance agent should be able to help with this.

In Conclusion

Homeowners insurance is a very complex topic but that doesn’t mean you shouldn’t understand the benefits and drawbacks of owning a policy.

Rising material costs, changing weather patterns, and escalating real estate prices make carrying a homeowners insurance policy a good idea even if it’s not required. Not to mention the peace of mind you’ll gain by knowing you are covered.